Insuring your business can be a big expense. Shopping around or working with a broker can help, but Washington has one type of insurance that can only be bought from the state – workers’ comp.

Workers’ comp insurance in Washington only comes from The Department of Labor & Industries (L&I). You can’t buy it from any other insurance company, even if you already have a workers’ comp policy in another state. Your employees in Washington must be covered by your company’s account with L&I.

Claim-Free Discount

But there is a secret to earning lower workers’ comp rates in Washington and it all starts with safety. It’s called the Claim-Free Discount and L&I offers it to any company that goes three years or more:

- Without any accidents at all

OR

- With only minor accidents that don’t trigger certain types of claim costs

You’re probably familiar with these types of discounts from your own auto or home insurance – many companies offer a discount for “safe driving” or not having any claims. Similarly, the Claim-Free Discount from L&I helps employers save 10 to 15 percent each year on their workers’ comp insurance – larger employers can save even more!

The value of a Claim-Free Discount

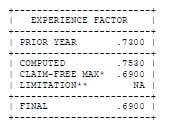

In this screen shot of one employer’s actual rate calculation, we can see they were already saving 27% percent a year (because they had a Prior Year Experience Modification Rate (EMR) rate of .7300, which is 27% less than the average rate of 1.00).

The computer had worked out a slight increase for them in the following year, to .7530, but the Claim-Free Discount kicked in and lowered their rate to .6900. This means they’re currently paying 4% less than they did last year, or an incredible 31% off of the average rate!

What does that mean in terms of money saved?

The Claim-Free Discount helps some companies save more than $1,000 per employee, per year over their competitors

Well, in transportation and warehousing, the average rate for workers’ comp in 2021 is $2.0370 — that’s per employee, per hour, all year long! So, the average company in this industry will pay $4,175.85 per full time employee for workers’ comp. insurance.

Thanks to this company’s Claim-Free Discount, they would multiply $4,175.85 by .6900, which comes out to $2,881.34 — a savings of more than $1,000 over their “average” competitor.

Losing the Claim-Free Discount

Meanwhile, a competitor who has experienced claims in the past three years may see their rates rise above average, increasing the advantage of the discount for your company.

Here’s an example of what it looks like when an employer loses their discount:

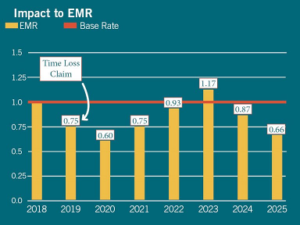

We can see that the employer was enjoying an increasing discount, with rates falling in 2018, 2019, and 2020, all the way down to .6000 (40% off average).

In 2021, however, the costs of a single claim began to be factored into this company’s rates. Their discount was taken away and replaced with the maximum possible rate increase, 25% per year.

Just one expensive claim can remove the discount and cause rates to double

As we can see, from just one claim, their rates will have nearly doubled by 2023. Their EMR of 1.17 means that they’ll end up paying 17% above average, a far cry from their 40% discount.

To put this in dollar terms, at roughly $2 per hour, a company that was paying $2,460 in 2020 will be paying $4,797 by 2025. That’s per employee, per hour.

How to earn and protect your Claim-Free Discount

As the name says, you can best protect your discount by being Claim-Free – this means preventing workplace injuries or long-term health conditions. At Approach, we have a safety team and ergonomic consultant available to help our clients build safe and effective work practices.

Claims are Okay

If an injury does happen, don’t worry! Just because a claim is filed doesn’t mean that your company will lose its discount.

- Claims that only incur medical costs won’t count against your Claim-Free Discount

- Light-duty work or kept-on-salary (in which your employee receives their usual pay while off work) can also protect your discount to avoid any indemnity costs

Just let your Retro Coordinator at Approach know as soon as an accident occurs. This way we can help you manage the claim right away and reduce the chance that your discount will be impacted.

Are you already earning the Claim-Free Discount?

You may already have the Claim-Free Discount. Or your company may be a year or two into the process of earning it. To find out the status, contact your Approach retro coordinator. We can also provide an account review, to see if any action is needed before L&I checks your account in early June to begin setting the 2022 experience modification rates.

Read more on The Basics of The Claim-Free Discount